If you've been working as an employee here for a while, you've seen the line on your payslip: Rentenversicherung. A slice of your gross income goes into Germany's state pension system every month, matched by your employer. It's automatic, compulsory for most employees, and easy to forget about.

Here's what it actually adds up to: the Standardrente, the pension you'd receive after a full 45-year career at average German wages, is about €1,913 per month as of July 2026. Think of that as the middle of the range, not the top. It's the figure for an average earner with a full career. Earn above average and you land higher (high earners with long careers can reach roughly €3,800), while people with career gaps, part-time years, or below-average pay land lower. And if you moved to Germany in your 30s, you'll accumulate far fewer contribution years, which means a proportionally smaller payout.

The gap between what you're used to earning and what the state actually pays - the Rentenlücke - is where private pension insurance comes in. This guide walks you through what it is, how it works, and who it actually makes sense for.

What is private pension insurance?

Germany's retirement system is built on three pillars:

There are two main formats:

Unlike the state pension, there's no minimum contribution period, (mostly) no government involvement, and no requirement to have worked in Germany for any set amount of time. It's fully in your control.

Why isn't the state pension enough?

Germany's state pension works on a points system. Each year you work and contribute, you earn *Rentenpunkte* based on how your income compares to the national average. At retirement, those points are converted into a monthly payment using the current pension value.

The current *Rentenniveau* (the official replacement rate) sits at 48%, and the government has committed to keeping it there until at least 2031. That means the standard pension replaces roughly half of average pre-retirement income, but only for someone who worked a full 45-year career at average German wages.

A few things make this especially relevant for expats:

You probably won't have a full contribution period.

If you moved to Germany in your 30s, you might accumulate 20 or 25 years of German pension contributions before retirement, not 40 or 45. Fewer years means fewer points, which means a smaller monthly amount.

Self-employed people may not contribute at all.

Freelancers and the self-employed are generally not required to pay into the statutory system. If you haven't been making voluntary contributions, your state pension entitlement could be minimal or zero.

Higher earners face a cap.

The state pension has a contribution ceiling (Beitragsbemessungsgrenze) of €8,450 per month / €101,400 per year in 2026. Contributions above that don't count toward pension points. If your income is well above average, the gap between your current lifestyle and your future state pension is proportionally even larger.

Who should consider private pension insurance?

Private pension insurance isn't for everyone, and it's worth being honest about when it makes sense and when something else might serve you better.

Situations where private pension insurance tends to be a strong fit:

You're self-employed or freelance.

With no employer-linked pension and often no mandatory state pension, private pension insurance is one of the primary tools for building retirement savings independently.

You want flexibility.

No contribution minimums, no strict restrictions on payout structure, and most plans are portable abroad. If your long-term plans in Germany are uncertain, that matters.

You want to supplement your bAV.

Company pension plans are great, especially when your employer contributes. But contribution limits apply and not every employer offers a strong plan. Private pension insurance is a natural complement.

You've already used your Rürup / Riester options and want a flexible additional layer.

With the Riester-Rente being phased out (more on that below), the private pension and the upcoming Altersvorsorgedepot are the main remaining options in the third pillar.

When is it probably not the right first move?

If your main goal is a large tax deduction on contributions today, the BasisrenteRürup is more efficient. If you're looking for state-subsidized investing with access to ETFs, the new Altersvorsorgedepot (launching January 2027) may be worth looking at first. Private pension trades some of those upfront benefits for control and flexibility. That trade-off is worth it for the right person, but it isn't automatically the default.

How does the payout actually work, and what about taxes?

The short version: private pension payouts in Germany get favorable tax treatment compared to most investment income. How favorable depends on whether you take a monthly pension or a lump sum.

If you take a monthly pension

The *Ertragsanteilsbesteuerung* applies. Only a portion of your monthly payment is taxable - specifically the *Ertragsanteil* (earnings portion), which is a fixed percentage based on your age when payments start. According to §22 EStG:

In practice: if you receive €1,500/month from your private pension at age 67, only €255 of that is added to your taxable income each month. For most retirees with modest other income, this means very little additional tax, sometimes none at all if you're below the basic allowance threshold.

If you take a lump sum

There's a favorable rule often called the "12/62 rule":

Example: you paid in €100,000 over the years and your plan is now worth €180,000. The €80,000 gain gets halved to €40,000 of taxable income. For someone in a lower income bracket at retirement, that's quite manageable.

If neither condition is met (contract under 12 years, or you're under 62), the full gain is taxed at the flat capital gains rate (*Abgeltungsteuer*) of 26.375%, which breaks down as 25% capital gains tax plus 5.5% solidarity surcharge (per §20 EStG). Still not catastrophic, but less favorable than the 12/62 route.

What about the new Altersvorsorgedepot?

This is the biggest change to Germany's private pension landscape in two decades, and it's worth understanding how it fits alongside private pension insurance.

The Altersvorsorgedepot (retirement savings depot) is a new state-subsidized investment account. The Bundestag passed the Altersvorsorgereformgesetz on March 27, 2026, and the Bundesrat approved it on May 8, 2026. It launches on January 1, 2027 and replaces the Riester-Rente.

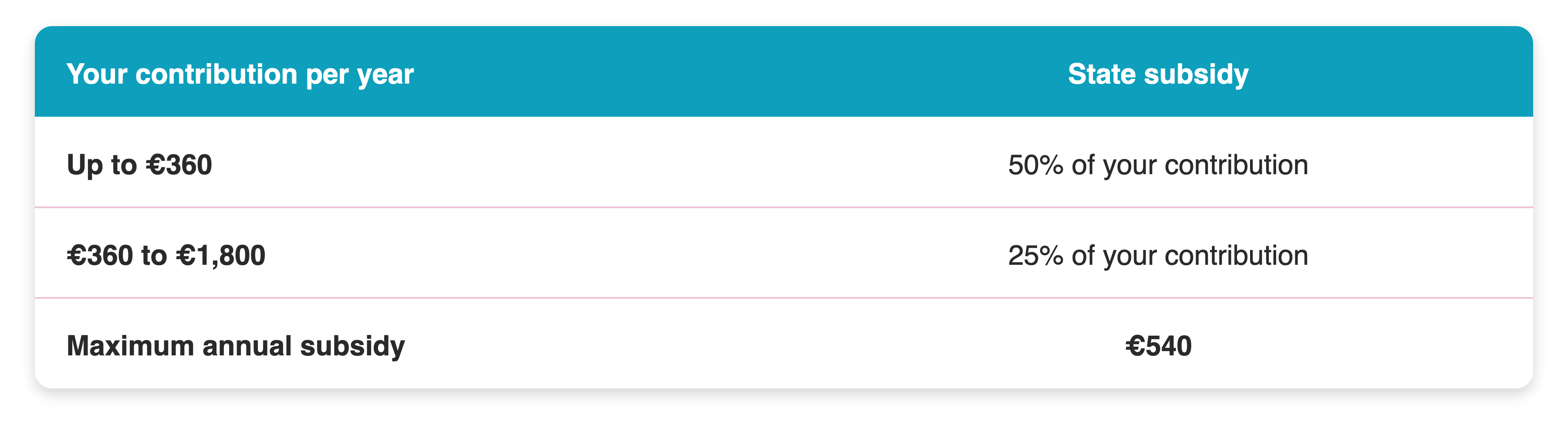

How the subsidy works

Unlike the old Riester flat allowance, the Altersvorsorgedepot uses a proportional subsidy:

For parents, the deal is even more generous: the state matches 100% of contributions up to €300 per year per child.

You can invest in ETFs and funds directly (risk categories 1-5 out of 7), with no capital guarantee requirement. There's also a Standarddepot option with pre-configured funds and a hard 1% cost cap for providers. Capital gains are tax-free during the savings phase.

How does this compare to private pension insurance?

The key difference is taxation at payout. The Altersvorsorgedepot uses downstream taxation (nachgelagerte Besteuerung), meaning payouts in retirement are fully taxed at your personal income tax rate, just like the state pension.

Private pension insurance, by contrast, benefits from the Ertragsanteil system, where only a fraction of each monthly payment is taxable. For many retirees, that results in significantly lower tax on payouts.

Which is better?

They serve different purposes:

They're not mutually exclusive. You can hold both, and for many expats, a combination may make the most sense.

Who qualifies?

Employees, civil servants, self-employed people (who file annual tax returns and are under 67), students with part-time jobs paying into statutory pension, and recipients of Arbeitslosengeld I. German citizenship is not required - you need to be subject to German income tax and be a mandatory member of a statutory pension system or meet specific eligibility criteria.

Frequently asked questions

Yes. What counts is residency in Germany, not nationality. Most German insurance companies offer plans to foreign nationals working and living in Germany without restrictions.

Most private pension plans continue running normally regardless of where you live. You keep contributing if you choose to, and at retirement age, you receive your payout, typically to any bank account worldwide. Some insurers may apply German withholding tax on cross-border payouts depending on the tax treaty between Germany and your country of residence. Worth checking the specific contract terms before signing.

Yes, and it's common. A typical setup: bAV through your employer for the contribution match, Rürup for the tax deduction (especially if self-employed), and private pension for flexibility and payout options. From 2027, you can add the Altersvorsorgedepot for state-subsidized ETF investing on top. There are no rules against layering these products.

Existing Riester contracts continue to run and can still receive contributions and subsidies after 2027. You can voluntarily transfer your Riester balance to a new Altersvorsorgedepot, but that decision should be evaluated individually. The mechanics of the transfer, including tax implications and rules for people close to retirement, vary by situation.

Yes. Many traditional German pension plans front-load their costs spread across the first five or so years. These reduce early growth significantly. Modern unit-linked plans backed by ETFs tend to have more transparent and lower fee structures. Comparing the actual cost structure of a plan is as important as comparing the investment strategy, arguably more so over a 20-year horizon.

It depends on the contract. Most plans include a death benefit, typically either returning your accumulated capital to a designated beneficiary or paying a survivor's pension. You name the beneficiary directly in the contract, and it's worth making sure this is set up correctly, particularly if you're not married, since the default inheritance rules in Germany may not reflect your wishes.

Need help deciding?

Choosing a private pension plan in Germany means comparing dozens of providers, fund strategies, and contract structures, mostly in German, and with long-term consequences that are easy to miss.

As independent insurance brokers, we compare plans across the market and help expats find the right setup for their situation: whether that's a standalone private pension, a combination with bAV or Rürup, or figuring out how the new Altersvorsorgedepot fits into the picture. No ties to any single provider, always in English.

Drop us a message and we'll help you figure out what actually makes sense for your situation.

Daniel Weiss

Email: daniel.weiss@versicherungsbuero-weiss.com

Telefon: +49 30 - 40 36 31 95 1

Mobil / WhatsApp : +49 178 - 140 584 0

Book a free consultation: https://calendly.com/vb-weiss_daniel/meeting