If you work for a German employer you are entitled to an employment-based retirement plan, also know as betriebliche Altersvorsorge (bAV). If you have never set up a bAV plan, there's a good chance you're missing out on an actual employer contribution on top of what you earn every month as well as a tax break. Not a hypothetical amount - a real percentage of your contributionthat your employer is required by law to add.

bAV is Germany's workplace retirement system and it comers in a few variations. Over half of all socially insured employees participate, according to figures from the aba (Arbeitsgemeinschaft für betriebliche Altersversorgung). Those who don't include a disproportionate number of expats who either haven't heard of it or assumed it didn't apply to them.

This guide explains how bAV works, what the real numbers look like in 2026, and what you need to know as someone who may or may not spend their entire career in Germany.

What is the Betriebliche Altersvorsorge?

Betriebliche Altersvorsorge is Germany's occupational pension system. It sits between the state pension (first pillar) and private pension plans like Riester or Rürup (third pillar) as the second pillar of German retirement provision.

The basic mechanic: instead of receiving part of your salary in cash, you redirect it into a pension plan before it gets taxed. Your employer is legally required to add their own contribution on top. The whole amount grows tax-deferred until you retire.

It is often compared to a 401(k) in the United States, and the analogy is reasonable up to a point. Both use pre-tax salary deferrals with employer matching. The German version is more tightly regulated, with mandatory minimum employer contributions, strict portability rules, and deferred taxation on the way out.

Why does this matter for expats?

Germany's statutory pension (gesetzliche Rentenversicherung) is calculated based on your contribution history. For someone who has spent their entire career here, it provides a meaningful but partial income in retirement.

For expats, the numbers are typically lower. According to Deutsche Rentenversicherung, the average monthly old-age pension varies significantly by gender and region, with men in western Germany receiving roughly €1,170 per month as new retirees. If you've only been contributing to the German system for 10 or 15 years, your entitlement will be smaller still.

The bAV doesn't fully close the retirement income gap on its own, but the combination of tax savings today and mandatory employer contributions makes it one of the most efficient ways to build supplementary retirement savings while you're here.

How do the savings work?

There are two layers to the financial benefit: the tax savings on your contributions and the mandatory employer match. Together, they make bAV significantly more effective than simply saving the same amount on your own.

Tax and social security savings

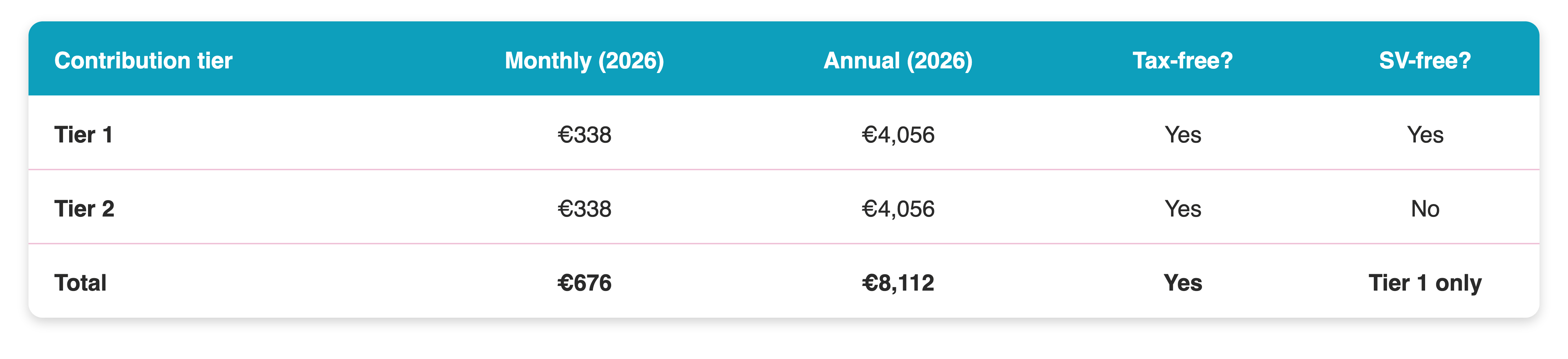

You can contribute up to 4% of the so-called annual pension contribution ceiling (Beitragsbemessungsgrenze, or BBG) completely free of income tax and all social security contributions. In 2026, the [pension BBG is €101,400 per year](https://www.bundesregierung.de/breg-de/aktuelles/beitragsgemessungsgrenzen-2386514), which means this threshold works out to €4,056 per year (€338 per month).

On that first €338 per month, you save income tax and the combined employee social security contributions (pension, health, long-term care, unemployment), which together amount to roughly 20% of gross salary.

You can contribute an additional 4% of the BBG (another €338 / month) with income tax exemption only. Social security contributions still apply to this portion, but the income tax saving alone is meaningful, especially at higher income levels.

The combined picture for 2026:

Your employer's mandatory contribution

Since January 2022, every employer in Germany is legally required to add a minimum of 15% to any bAV deferred compensation contribution.

The logic: when you defer part of your salary, your employer saves on social security contributions for that portion. German law requires them to pass at least 15% of your contribution back to you as an employer top-up.

If you contribute €338 / month, your employer must add at least €51 / month on top. That is not deducted from your salary - it is extra. Many employers contribute more than the 15% minimum, especially if their actual SV savings exceed that threshold.

What happens when you retire?

Private pension insurance isn't for everyone, and it's worth being honest about when it makes sense and when something else might serve you better.

Situations where private pension insurance tends to be a strong fit:

When can you start receiving payments?

The earliest payout age for bAV plans is currently 62 (for contracts signed after 2012). Standard retirement age in Germany for anyone born in 1964 or later is 67. Most policies let you choose between a monthly pension, a lump sum, or a combination - the exact options depend on your specific plan and provider.

How are bAV payouts taxed?

The defining principle is deferred taxation (Nachgelagerte Besteuerung): contributions go in tax-free, payouts at retirement get taxed as regular income.

This still usually comes out ahead because most people are in a lower income tax bracket in retirement than during their working years. The tax-free compounding over decades also means the invested sum grows faster than it would in an after-tax savings account.

What about health insurance deductions?

If you are a member of the statutory health insurance (GKV) when you retire, your bAV pension payout will be subject to health insurance and long-term care contributions.

Important: there is a monthly exemption. Since January 2020, a Freibetrag applies to bAV payouts. In 2026, this exemption is €197.75 per month. Only the portion of your monthly bAV pension that exceeds this amount is subject to GKV contributions. For smaller and medium-sized company pensions, this exemption significantly reduces (or even eliminates) the health insurance bite. This was a major reform that made bAV considerably more attractive for the average employee.

If you are privately insured (PKV) at retirement, this GKV deduction does not apply at all. For expats who transition to PKV, one of the most commonly cited drawbacks of bAV effectively disappears.

What if your situation changes?

Changing jobs

Your own contributions are always yours. Any salary you have deferred into a bAV plan is your money from day one and cannot be forfeited.

Employer contributions vest after 3 years. If you leave a company before the bAV plan has been running for 3 years, the employer-added contributions may not be fully yours yet. This vesting period was reduced from 5 years to 3 by the Betriebsrentenstärkungsgesetz in 2018. But this also depends on exactly how your employer has setup up the bAV and nowadays, many employers let you take their contributions with you a lot earlier.

When you move to a new employer, you can transfer the accumulated value to a plan there and continue contributing (Übertragung), or keep the existing plan as a paid-up policy that continues growing. Direktversicherung policies are the most straightforward to transfer. Your broker can help with the paperwork, and it is usually not complicated.

Leaving Germany

This is the question we hear most often from expats weighing whether bAV is worth starting at all. The short answer: leaving Germany does not mean losing what you have built.

Your accumulated bAV value stays invested and keeps growing. When you reach the minimum payout age (62 at the earliest), you receive your pension regardless of where you live. A few things worth knowing before you go:

Is bAV worth it?

For most people with a German employment contract, yes, and particularly at Tier 1. The combination of income tax savings, social security savings, and a mandatory minimum 15% employer match creates an immediate effective return that is difficult to match with any other savings product.

Some caveats to remeber:

Short stays in Germany limit the benefit. If you are here for less than two or three years, the startup costs of some older-style whole-life policies, combined with the 3-year vesting cliff on employer contributions, can offset the savings. More modern policies have lower upfront costs, but it is worth checking the specific terms.

Employer contributions vary significantly. The 15% minimum is just a floor. Most employers contribute substantially more, with many simply doubling what you put in. Always ask what your employer's actual contribution rate is.

Frequently asked questions

There are five legal forms of bAV in Germany: Direktversicherung, Pensionskasse, Pensionsfonds, Direktzusage, and Unterstützungskasse. As an expat at a small or medium-sized company, you will almost certainly encounter the Direktversicherung. It's the most common, most portable, and the one every employer is required to offer if you ask. Larger corporations like Volkswagen or Siemens sometimes use Direktzusage (a direct commitment from the company balance sheet), but the tax rules are broadly similar regardless of the form.

Yes. Every employee in Germany has the legal right to request a Direktversicherung through salary deferral (Entgeltumwandlung). Your employer cannot refuse. They are not required to set one up without being asked, but they must offer it on request.

Generally yes. Part-time employees have the same rights as full-time employees, proportionally. For fixed-term contracts, you can participate for the duration. If your contract ends before the 3-year vesting period, you may not have full entitlement to the employer-added contributions.

Your plan does not disappear. You can continue making private contributions (without the employer match) or (temporarily pr permanently) stop contributing and let the policy become a paid-up plan. The accumulated value stays in place and continues to grow. Early withdrawal is generally not an option.

Yes. You can usually adjust your contribution amount once per year, up to the annual maximum of €8,112 (2026). Some employers restrict the timing of changes, so check your specific plan rules.

More attractive. The GKV health insurance deduction on bAV payouts at retirement does not apply for PKV members. For higher earners who are in or plan to move to private health insurance, bAV becomes a more straightforward win.

These are separate products. bAV is the second pillar (employer-linked), while the Altersvorsorgedepot is a third-pillar private pension product. You can have both simultaneously, and the contribution limits are independent of each other. The Altersvorsorgedepot launches January 1, 2027; bAV rules are unaffected by that change.

Need help deciding?

Choosing the right bAV plan comes down to comparing providers, understanding fee structures, and making sure your employer's offering is actually competitive. That's a lot of moving parts, especially when the German system is not your home system.

As independent insurance brokers, we compare plans across the market and help expats and international professionals find the right setup for their situation - always in English. If you want to check whether your current bAV plan holds up, explore better options, or set one up from scratch, drop us a message. That's exactly what we do every day.

Daniel Weiss

Email: daniel.weiss@versicherungsbuero-weiss.com

Telefon: +49 30 - 40 36 31 95 1

Mobil / WhatsApp : +49 178 - 140 584 0

Book a free consultation: https://calendly.com/vb-weiss_daniel/meeting