Starting January 1, 2026, the income threshold for switching to private health insurance will rise significantly, making it harder for high earners to make the transition.y is becoming more challenging. Starting January 1, 2026, the income threshold for switching to private health insurance will rise significantly, making it harder for high earners to make the transition.

Here is everything you need to know about the changes, how they affect you, and what you can do about it.

What's changing in 2026?

The German Federal Council (Bundesrat) has officially approved the new social security thresholds for 2026. Several key insurance thresholds will increase substantially in 2026:

What this means for you?

If you're a high earner in Germany, these changes have direct financial implications:

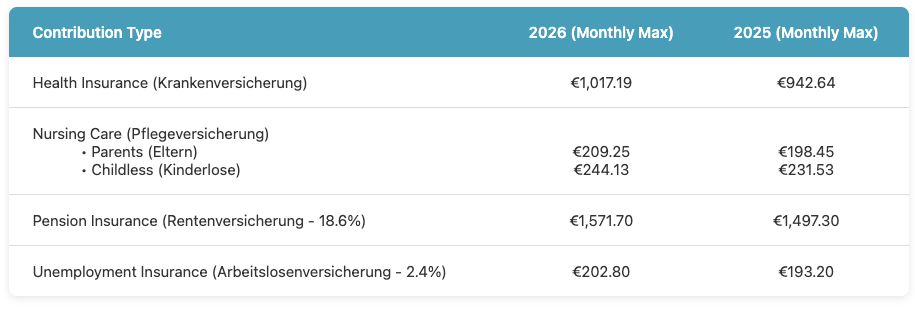

When you add contributions for long-term care, pension, and unemployment insurance, the total monthly burden officially breaks the €3,000 mark: approximately €3,018 for parents or €3,053 for those without children

Understanding the numbers

Here's a clear comparison of the key thresholds:

Based on current rates, here's what those at the ceiling will pay:

These calculations assume current contribution rates, which may change. The average additional health insurance contribution has already been exceeded by many public health insurance providers earlier this year, with this trend continuing.

What should you do?

If you're considering switching to private health insurance, these changes make planning even more important. The decision between public and private insurance is complex and depends on many factors beyond just your income, including your age, health status, family situation, and long-term career plans.

You can read more about Private Health Insurance here.

Our advice: Don't rush this decision. The German insurance system offers different advantages depending on your individual circumstances. Private health insurance can offer excellent coverage and cost savings for some people, but it's not the right choice for everyone.

If you're approaching the income threshold or have questions about whether private health insurance makes sense for your situation, we're here to help.

We specialize in guiding expats and international professionals through these complex decisions, always with transparent, independent advice in English.